15th April 2026 By Paul Yandall | paul@propertyticker.co.nz | @propertyticker

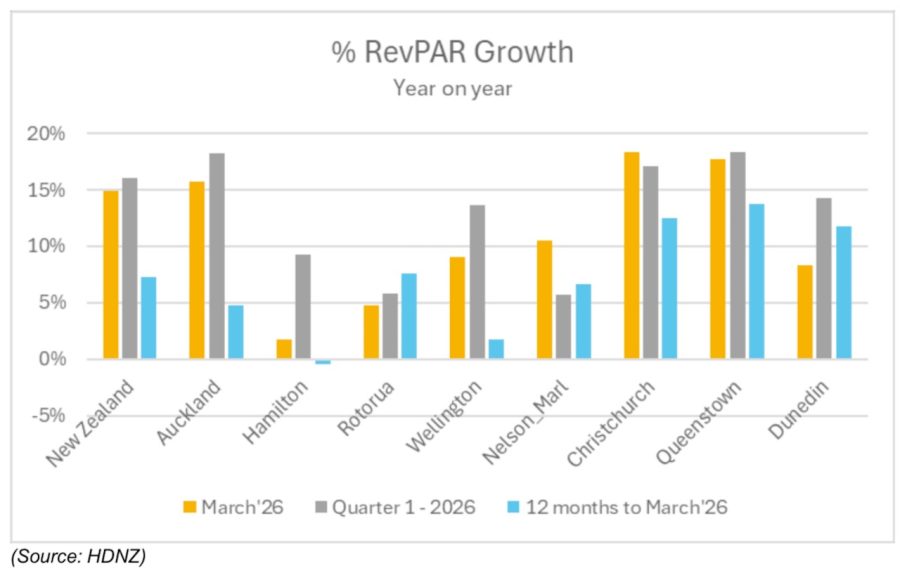

Auckland, Christchurch and Queenstown’s hotel markets reported double-digit revenue per room growth in March 2026, despite war in the Middle East breaking out at the end of February.

Horwath HTL said in its latest New Zealand Hotel Performance Focus for March and Q1 2026, that the country’s hotel market finished the first three months of the year, “with no material signs of demand weakness following world events that started on 28 February and a 14.9% year-on-year increase in national RevPAR”.

“Despite geopolitical tensions in the Middle East that escalated in late February, overall arrivals were not materially disrupted,” stated the report, authored by Horwath HTL directer Wim Ruepert.

“The primary observable impact was a decline of approximately 87% in arrivals from the UAE and Qatar, which was offset by increased arrivals from Singapore and Malaysia.”

The consultancy’s analysis of Hotel Data New Zealand figures from Hotel Council Aotearoa showed Christchurch recorded the strongest monthly RevPAR growth, up 18.3% on March last year.

“ADR growth of 12.3% in Q1 was the second highest nationally, while occupancy reached 90% for the quarter, the highest of any major market,” Horwath HTL said.

“The primary driver was a 21% year-on-year increase in international arrivals at Christchurch Airport in Q1, the vast majority of which originated in Australia.”

Queenstown delivered an “outstanding performance”, with RevPAR up 17.7% year-on-year, driven by ADR growth of 15.3%.

“Hotels reported a notable shift towards Asian visitors, with increased representation from China, Japan and other Asian countries, and a slight decline in the shares from Australia and the United States,” Horwath HTL said.

Auckland’s hotel market reported March RevPAR up 16.7% year-on-year.

“The strong demand increase has largely absorbed the approximately 1,300 additional rooms added to the Auckland market since April 2024.

“The pace of supply growth has, however, constrained rate recovery: ADR is lagging 2024 levels across all hotel categories.”

Wellington’s hotel market lagged other regions but still saw RevPAR up 9% in March and 13.6% in Q1.

“Despite this, Wellington remains the only major key market where first-quarter RevPAR is still below Q1 2019 pre-Covid levels, trailing by approximately 2%.”

Horwath HTL’s latest New Zealand Hotel Performance Focus can be read here.

23 Mar 2026 Owner of award winning hotel in liquidation

Subscribe to The Yield newsletter. Get the latest commercial property news and insights delivered to your inbox every morning.